by TIAN Heqi

China's listed rare earth companies posted strong profit growth in 2025, helped by tightening state control over supply, rising export restrictions and booming demand from electric vehicles, wind power and robotics.

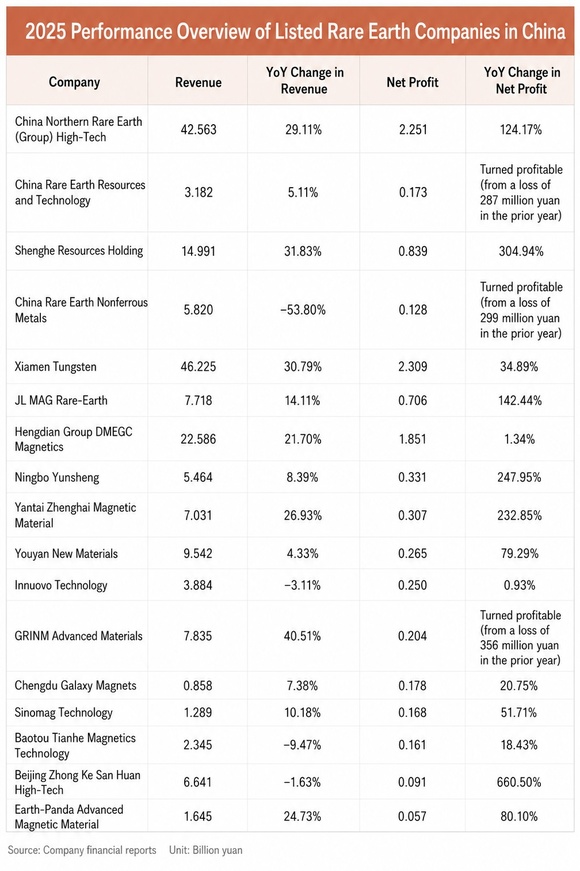

Jiemian News tracked 17 listed companies across the rare earth supply chain, all of which reported higher earnings. Xiamen Tungsten Co led the sector with net profit of 2.31 billion yuan (US$339 million), followed by China Northern Rare Earth (Group) High-Tech Co at 2.25 billion yuan and Hengdian Group DMEGC Magnetics Co at 1.85 billion yuan.

Rare earth magnet makers outperformed. Beijing Zhong Ke San Huan High-Tech Co posted a 660.5% jump in net profit, while Ningbo Yunsheng Co and Yantai Zhenghai Magnetic Material Co both reported gains of more than 200%. JL MAG Rare-Earth Co also more than doubled earnings.

China Rare Earth Resources and Technology Co, China Rare Earth Nonferrous Metals Co and Jiangsu Huahong Technology all returned to profit after earlier industry downturns.

The earnings rebound reflected tighter supply controls and stronger downstream demand.

China tightened production quotas and export controls over strategic minerals. Since the third batch of quotas announced in December 2023, only two state-backed groups — China Rare Earth Group and Northern Rare Earth — have received mining and smelting quotas from the Ministry of Industry and Information Technology, according to Jiemian News research.

China also introduced stricter rules governing total rare earth mining and smelting volumes, bringing imported ore processing into the regulatory system and establishing traceability mechanisms.

In April 2025, China's Ministry of Commerce and General Administration of Customs announced export controls on some medium and heavy rare earth-related items. Additional controls on rare earth technologies followed in October, underscoring Beijing's increasingly tight grip over strategic mineral resources.

According to a Goldman Sachs report, China controls 69% of global rare earth mining, 92% of refining and 98% of magnet manufacturing.

Supply was also disrupted overseas. Political instability and environmental restrictions in Myanmar, together with Vietnam's export controls on raw ore, tightened imports of medium and heavy rare earth materials. Overseas refining projects face long expansion cycles, making short-term alternatives difficult.

Myanmar, the world's third-largest rare earth ore producer, has become China's largest source of imported rare earth feedstock. Data from Antaike showed Myanmar accounted for 56% of China's rare earth raw material imports in 2025, while Laos contributed 25% and the United States accounted for 19%.

China imported 23,000 tonnes of rare earth metal ore from the U.S. in 2025, down 57.6% year on year. Previously, the U.S. accounted for nearly all of China's imported rare earth concentrate supply.

Demand from electric vehicles and advanced manufacturing also strengthened.

Rapid EV sales growth boosted demand for neodymium-iron-boron magnets used in electric motors, while rising wind-power installations increased demand for permanent magnet generators.

A report by Guotai Haitong Securities estimated that EVs and new wind-power installations consumed 63,000 tonnes of rare earth magnetic materials in 2024, accounting for 24% of China's total demand. That share is expected to rise to 28% in 2025 and 31% in 2026.

Emerging sectors such as humanoid robotics, eVTOL aircraft and energy-efficient industrial motors also became new demand drivers.

JL MAG said its robotics and industrial servo motor business generated 300 million yuan in revenue in 2025, up 45.2% year on year. The company has built automated rotor production lines for humanoid robots and begun small-batch deliveries.

Industry estimates suggest each humanoid robot requires about 4 kilograms of neodymium-iron-boron magnets, implying demand of roughly 20,000 tonnes if production reaches 5 million units.

After years of inventory reductions since 2022, supplies of products such as praseodymium-neodymium oxide and terbium oxide remained low, amplifying price gains in 2025.

Rare earth concentrate prices rose for seven consecutive price adjustments. On April 11, Baotou Steel Union and Northern Rare Earth said second-quarter 2026 transaction prices for rare earth concentrate would rise 44.6% from the previous quarter to 38,804 yuan per tonne excluding tax, the biggest quarterly increase since the pricing mechanism was overhauled in 2023.

Shanghai Metals Market (SMM) data showed average prices for praseodymium-neodymium oxide reached about 488,100 yuan per tonne in 2025, up 52.4% during the year and 24.4% higher than the previous annual average.

Momentum carried into 2026. In the first quarter, China Rare Earth posted a 90.8% increase in net profit, while Northern Rare Earth's earnings more than doubled.

China's latest 15th Five-Year Plan also highlighted the need to strengthen competitive advantages in rare earths, rare metals and superhard materials, signaling continued policy support for the sector.

Analysts said tighter supply-demand balances and policy backing could keep prices firm despite concerns over whether downstream users can absorb higher prices.